The Reopening Era May Finally Be Here, But Risks Still Remain

The Reopening Era May Finally Be Here, But Risks Still Remain

Investors and global citizens alike are now over a year removed from the initial COVID-19 scare that shuttered businesses, brought economic activity across the globe to a halt, and caused a shift in human habits and interactions. Now, after a year that was, at minimum, challenging, the vast majority of signs are pointing to the outcome we’ve all been patiently waiting for: life returning to “normal”. While the economic future does look bright, investors should still be aware of risks that remain and understand the road to normalcy may still be bumpy.

Current estimates indicate the potential for herd immunity in the U.S. and a return to “normal” by mid-summer 2021. This does seem reasonable given the rate of vaccination in the U.S. coupled with the modest new case count seen over the last two months. The risks? Vaccines are only temporary with most studies suggesting immunization via vaccine will last anywhere from 6 months to 2 years. We also know there have been reported cases in already-vaccinated people, although rare in occurrence and less severe. Lastly, we’ve learned COVID-19 does not alter its timeline to match our forecasts and expectations. Last March, many of us expected this would be a temporary hiccup in normal life, only to have our forecasts for normalcy pushed back time after time.

Confirmed New U.S. Cases (7 day moving average)

U.S. Vaccination Data

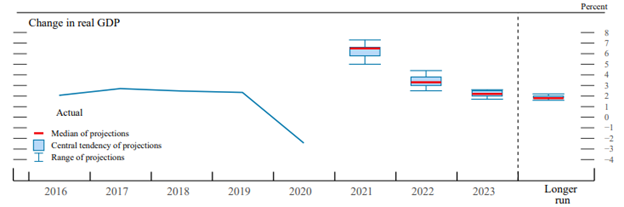

With the understanding of the current COVID-19 situation, the next area of focus for investors should be the economic recovery in the U.S. As was expected, the pandemic-fueled 2020 made a dent in GDP growth and caused a massive spike in unemployment. 2021 GDP forecasts are assuming a massive rebound in economic activity and hiring. Most forecasts predict a rise of 6%-8% in U.S. GDP growth in 2021 with unemployment seen falling to 4% or below by year-end. When combined with 20%-30% forecasted growth in earnings for S&P 500 companies, surging retail sales (up almost 10% in March), a record level of fiscal stimulus roaring through the economy, and built up consumer savings, a reopening in 2021 looks promising and prosperous.

The risks to this economic boom lie just below the surface. GDP is comprised of four main metrics: consumer spending, government spending, business spending, and net imports/exports. Any hiccup in consumer spending, business hiring, or any inefficient government spending that does not augment growth could create serious downside growth surprises. Further, the proposed corporate tax increase from the Biden administration may disincentivize businesses from making large capital expenditures this year in the hopes that deferring them would reduce their taxable income in the future. The passage of this tax increase could also inhibit earnings growth. Lastly, if people’s long-term habits have indeed changed during the pandemic, the demand for traditional capital investment may suffer.

Source: Federal Reserve

Source: St. Louis Fed (FRED)

The preceding seems to indicate a bullish outlook for equity markets and perhaps a troubling outlook for bond markets. The combination of economic reopening, inflation uncertainty, interest rate volatility, and richly valued stocks in nearly every U.S. sector may mean the ride upward could be volatile. It’s also important to remember the market is forward-looking. The reopening was being priced into markets in mid-2020 and acting on newly released economic data or trends for short-term profits will likely result in disappointment.

10 year Treasury yields rose from 0.91% in January to almost 1.75% in mid and late March, only to fall back down to 1.54% the last couple of weeks. Investors were certainly at odds with the Federal Reserve, whose chair Jerome Powell has maintained the position that rates will remain low through 2022 and into 2023, waiting for inflation and employment to reach levels suitable for a rate hike. Investors seemed to disagree in Q1, sending those 10 year Treasury yields soaring, and both stocks and bonds falling. The Fed has also maintained inflation will increase, but this increase will be temporary.

Markets have been left to wrestle with their own predictions on what the future of bonds and equities will look like. The reopening momentum has certainly helped equities, with the S&P 500 up over 6% YTD through March, but the equity bull run looks a little different than last year with value and cyclical strategies now outgaining the darlings of 2020 comprised of stay-at-home and technology-driven stocks. The Russell 1000 Value index is up over 11% YTD, the recently beaten-down Financials sector is up over 16%, the Russell 2000 Index is up 12.70%, while the Russell 1000 Growth and NASDAQ indices are up 0.94% and 2.95%, respectively.

Bonds have certainly been feeling the pain from yield spikes. The Barclays US Aggregate Bond Index, often a proxy for U.S. bond investors, is down 3.37% on the year through March.

Optimistic economic data, vaccination data, and recent market momentum appear to create a promising environment for U.S. equities going forward. However, investors should still exercise caution partaking in the euphoria. The S&P 500 remains as richly valued as it has since the dot-com bubble of the late 90’s and these high valuations have historically indicated sub-par returns going forward.

Source: JPMorgan, FactSet

International developed markets as a whole appear attractively valued and may provide ample long-term diversification and return benefits to U.S.-centric portfolios despite possible short-term headaches associated with botched vaccine rollouts across Europe and continued Brexit uncertainties. Relative to U.S. markets, international markets appear to be on clearance, except you’re not getting last year’s fashion off the clearance rack, you’re getting an opportunity to buy something valuable at a discount. Below shows how cheaply priced international equities are compared to their U.S. counterparts based on the P/E ratios of the S&P 500 and MSCI ACWI ex-U.S. indices. As of March 31st, you can buy $1 in earnings of the international index for 25% less than you can buy $1 of earnings for the S&P 500.

Source: JPMorgan, FactSet

Long-term investors should remain invested, diversified, and not take any drastic actions out of short-term uncertainty or volatility. The simple fact is with all the unknowns still remaining in the economy and in markets, we will likely see short bursts of volatility in both interest rates and equity markets. We are coming off the largest and most unique crisis of our time. Markets will take their time to sort out the path forward and those that exercise patience and discipline will benefit long-term.

“Knowing that you don’t know is more useful than being brilliant” – Charlie Munger